France Launches a Price Offensive in the UK Wine Market and Lifts Exports 3%

France Gains Market Share with Price Cuts While Rivals Struggle to Maintain Sales Volumes and Revenues

2026-02-27

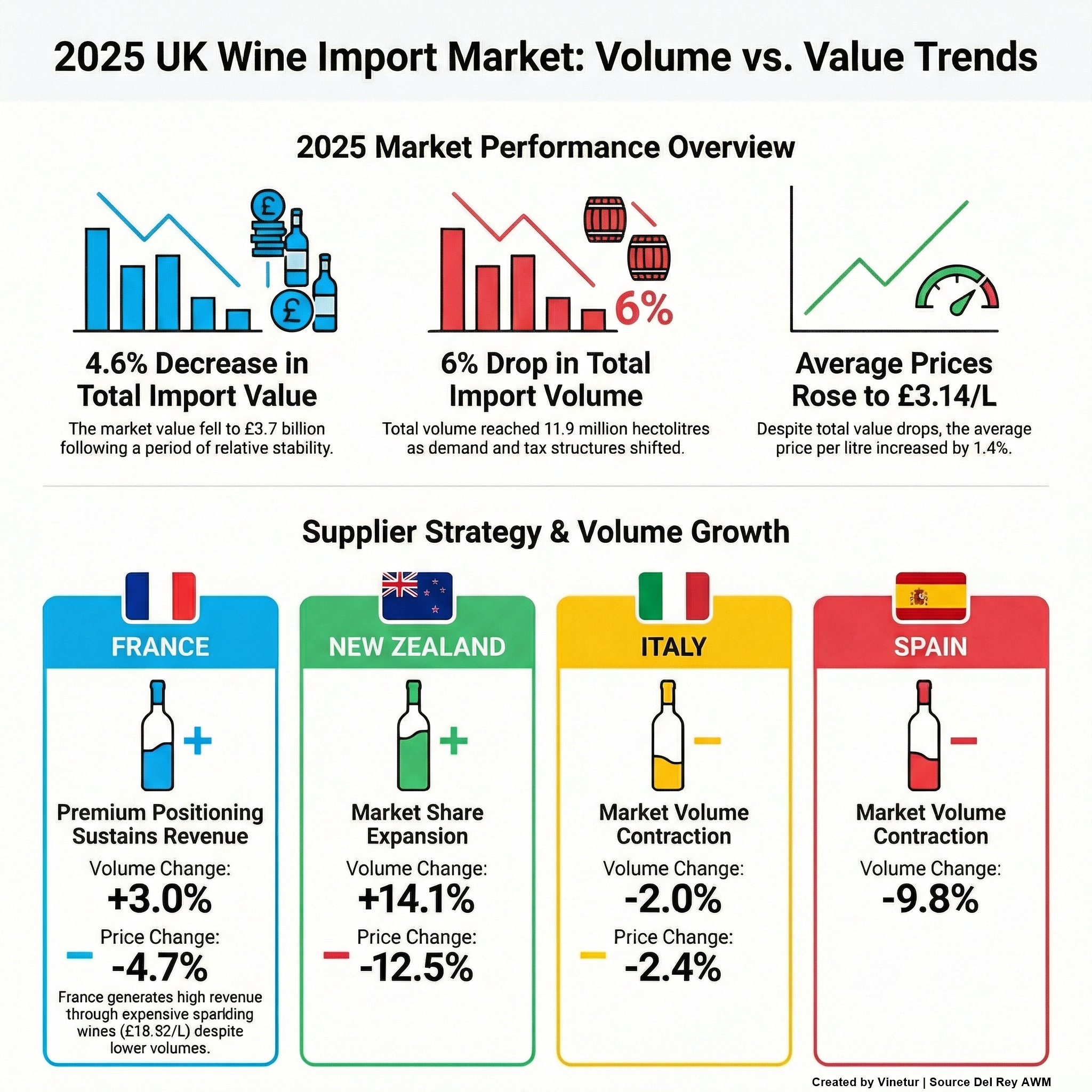

Wine imports into the United Kingdom declined in 2025, with both volume and value falling compared to the previous year. According to data from HM Revenue & Customs analyzed by Del Rey AWM, the total volume of imported wine dropped by 6% to 11.9 million hectoliters. The value of these imports decreased by 4.6%, reaching £3.7 billion. Despite these declines, the average price per liter increased slightly by 1.4% to £3.14.

This downturn follows a period of relative stability in the UK wine market in 2024. Analysts point to several factors behind the decline, including changes in the UK’s alcohol tax system and evolving consumer preferences. The new tax regime, which came into effect in early 2025, has altered pricing structures for alcoholic beverages and may have contributed to reduced demand.

The impact of these changes has not been uniform across all major wine suppliers to the UK. Among the top fifteen exporters, only France, New Zealand, and Portugal saw growth in sales volume. France increased its exports by 3% to 180 million liters, while New Zealand’s exports rose sharply by 14.1% to 86 million liters. Portugal posted a modest gain of 1.9%, reaching 26 million liters.

Other major suppliers experienced declines. Italy’s exports fell by 2%, Spain’s by 9.8%, Australia’s by 13.6%, Chile’s by 12.7%, and South Africa’s by 19.1%. Romania and Greece also saw smaller decreases of 1.7%. These figures reflect a challenging environment for many traditional wine exporters.

Price adjustments played a significant role in shaping these outcomes. France reduced its average export price to the UK by 4.7%, bringing it down to £7.74 per liter, while New Zealand cut prices even more steeply by 12.5% to £2.88 per liter. These reductions appear to have supported higher sales volumes for both countries.

However, not all suppliers benefited from lower prices. For example, Chile, Argentina, and Germany did not see improved sales despite price cuts, suggesting that other factors such as brand strength and market positioning are also important. Conversely, Australia and Spain raised their average prices in 2025 but saw corresponding drops in sales volumes.

In the sparkling wine segment, France remains a key player with premium products like Champagne commanding an average price of £18.52 per liter. Despite exporting only 27 million liters—far less than Italy’s 124 million liters—France generated nearly £493 million in revenue from sparkling wines, slightly ahead of Italy’s £440 million from Prosecco and other sparkling wines sold at an average price of £3.56 per liter.

Spain is the third-largest supplier of sparkling wines to the UK but lags behind both France and Italy in volume and revenue, selling just 14 million liters at an average price of £3.59 per liter for a total of £49 million.

In 2025, France reduced its average price for sparkling wines by over one pound per liter (a decrease of 5.2%), which led to a sales volume increase of more than 1.3 million liters or 5.2%. This resulted in stable revenues despite lower prices. Italy also lowered its prices by 4.1%, but this did not boost sales; shipment volumes dropped slightly by 0.7%, leading to a revenue decline of 4.8%. Spain took a different approach by raising its average price by 11%, which caused a larger drop in sales volume (down 4.4%) but still resulted in a revenue increase of 6.4%.

For non-sparkling bottled wines, France, Italy, and Spain together accounted for over two-thirds of both value and volume in the UK market last year. French wines commanded an average price of £5.91 per liter—more than double that of Italian (£2.80) or Spanish (£2.93) wines—allowing France to generate £879 million from non-sparkling bottled wine exports compared to Italy’s £431 million and Spain’s lower figures.

France again led with sharper price reductions (down 6.2%), which spurred a sales volume increase of 3.9% but only a minor revenue decline of 2.6%. Italy’s smaller price cut (down 1.5%) did not prevent a drop in both volume (down 2.3%) and revenue (down 3.7%). Spain made only minimal changes to pricing (down just 1%) but suffered a significant drop in shipment volumes (down 7.3%).

These results highlight different strategies among leading suppliers as they respond to changing market conditions in the UK wine sector: France has opted for more aggressive price reductions that have helped maintain or grow sales volumes with limited impact on revenues; Italy has taken a more cautious approach; Spain appears focused on maintaining or increasing prices even at the risk of losing market share.

The developments raise questions about how regulatory changes and shifting consumer trends are influencing pricing strategies among major wine exporters to the UK—and whether France’s approach will continue to deliver stronger results than those of its competitors as market conditions evolve further in coming years.

Founded in 2007, Vinetur® is a registered trademark of VGSC S.L. with a long history in the wine industry.

VGSC, S.L. with VAT number B70255591 is a spanish company legally registered in the Commercial Register of the city of Santiago de Compostela, with registration number: Bulletin 181, Reference 356049 in Volume 13, Page 107, Section 6, Sheet 45028, Entry 2.

Email: [email protected]

Headquarters and offices located in Vilagarcia de Arousa, Spain.